Nowadays, it seems everyone is drawn to high-risk investments—be it cryptocurrency, sports betting, or options trading with promises of hefty returns. However, if you prefer to minimize risk, you’re likely looking for investments that offer guaranteed returns, consistent monthly income, and protection against inflation. While inflation remained moderate for a while, it poses a significant risk historically and cannot be overlooked.

If a low-risk approach sounds appealing, consider reading “3 Ways to Build an Inflation-Adjusted Pension” by Allan Roth. This article highlights how Social Security functions in this manner and introduces a new line of LifeX Inflation-Protected Longevity Income ETFs.

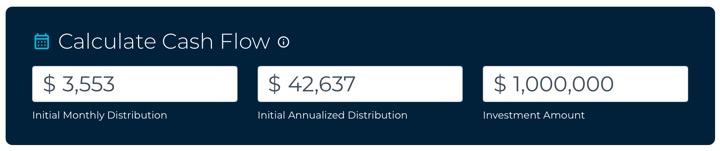

As of December 11, 2025, the LifeX 2055 Inflation-Protected Longevity Income ETF (LIAM) features a managed portfolio of U.S. Treasury Inflation Indexed Bonds (TIPS), promising a guaranteed real withdrawal rate of 4.26% for the next 30 years. This means that a $1,000,000 portfolio could provide approximately $42,600 in annual income this year, with yearly adjustments based on CPI inflation. Assuming an average inflation rate of 3%, the income in the 30th year could exceed $100,000 annually. However, inflation could potentially be higher, which is why private insurance companies typically avoid offering long-term inflation protection.

Keep in mind that after these 30 years, the initial investment will be depleted. Your annual income will essentially be a return of your principal.

The expense ratio for this ETF is 0.25%, which is manageable—not as low as Vanguard, but reasonable. I appreciate that it simplifies the investment process in a straightforward ETF structure, as creating a TIPS ladder on your own can be complicated (and not something you’d want to manage at 80 or 90). However, there’s a valid concern if you buy a 30-year ladder at age 65 and live beyond 95. It’s a possibility; hence, this product is ideally suited for risk-averse individuals seeking stability.

In summary, a TIPS ladder or a similar inflation-adjusted strategy could work well with a traditional annuity, such as a Single Premium Immediate Annuity (SPIA) or a deferred longevity annuity that kicks in later. While these don’t adjust for inflation, they can offer a higher initial fixed income for life. This is what I’ve arranged for my parents—Social Security that adjusts for inflation combined with a joint income annuity that continues for as long as one of them is alive.