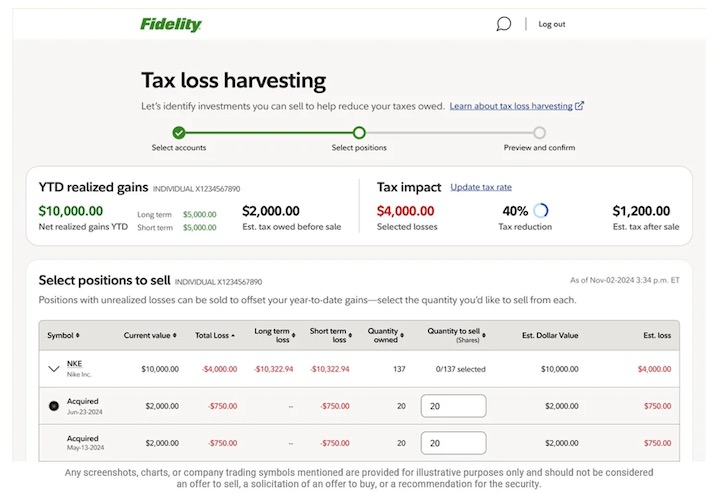

Fidelity offers a variety of useful Tools & Calculators, many of which are accessible to everyone. However, their Tax-Loss Harvesting Tool (login required) is specifically designed for Fidelity taxable brokerage clients. This tool uses your personal data to outline your expected capital gains for the year and assists in identifying potential capital losses that can be “harvested.”

You will need to input your marginal tax rates (you can estimate these based on current brackets). The tool simplifies the process further by allowing you to place (market) orders to sell shares with just a few clicks.

For a comprehensive guide on tax-loss harvesting, refer to Fidelity’s article, “How to Reduce Investment Taxes”:

Investment losses can be utilized in two main ways:

– Losses can offset capital gains.

– Remaining losses can be used to offset up to $3,000 of income on your tax return in a single year (the limit is $1,500 for married individuals filing separately).[…] Gains and losses fall into two categories: short-term and long-term.

– Short-term capital gains and losses occur from selling investments held for one year or less.

– Long-term capital gains and losses are realized from selling investments held for over one year.

The main difference between short-term and long-term gains lies in their tax rates.Short-term capital gains are taxed at your ordinary income marginal tax rate, which can be as high as 37%.

Important Note on Wash Sales: The tool may not account for all your non-Fidelity trades and does not include trades within tax-deferred accounts. If a wash sale happens, your loss may be denied. Here’s the advisory provided:

Wash Sale Advisory: Estimated savings from tax-loss harvesting assumes no wash sales that would defer your tax loss.

If you sell shares at a loss and then buy additional shares of the same or a substantially identical security within a 61-day window (30 days before and after the sale date), you may trigger a wash sale. If this occurs, the loss will be disallowed for tax purposes, and it will be added to the cost basis of your shares in that security. Fidelity adjusts cost basis information for any wash sales resulting from purchases of identical securities within an account.

You need to review your records across all Fidelity and non-Fidelity accounts to accurately account for any wash sales impacting your losses.

ETFs: A Simple Method for Tax-Loss Harvesting. Even if you follow a buy-and-hold strategy with ETFs, consider ETF tax-loss harvesting. You can realize a loss from the sale of an ETF and then quickly acquire a similar but not “substantially identical” ETF to avoid triggering a wash sale. This practice is now a common approach in the industry, and Fidelity has additional resources on this topic.

When assessing your ETFs relative to the wash-sale rule, analyze the issuer, index, and underlying holdings between the two ETFs. The greater the differences, the lower the likelihood of triggering a wash sale.

Even Vanguard employs ETF tax-loss harvesting strategies through the use of “surrogate ETFs.”

Surrogate funds are ETFs that Vanguard’s Personal Advisor uses to replace investments sold for loss harvesting. These are Vanguard ETFs® with comparable asset and sub-asset allocations to the funds being replaced.

There may be fewer chances to harvest tax losses this year, given that the market is generally up (a positive sign!), but it’s a consideration for future reference.

Please note: I do not offer legal or tax advice. The information presented here is general and for educational purposes only and should not be construed as legal or tax advice.